Mar, 23, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on March 23, 2026.

Mar, 20, 2026

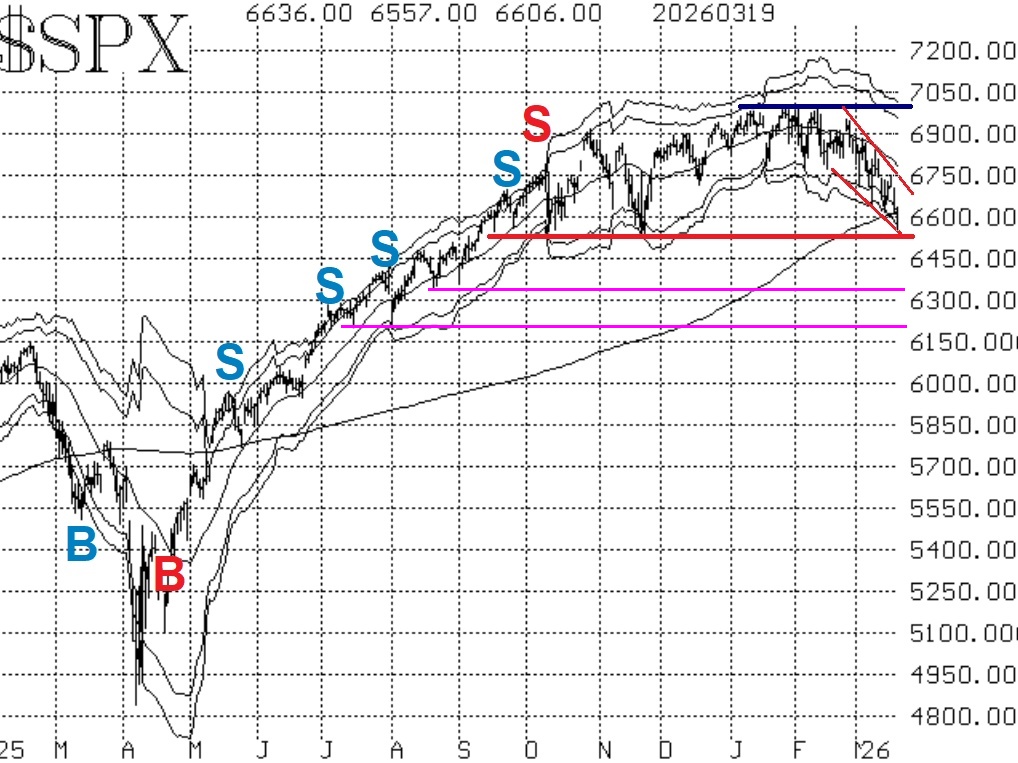

By Lawrence G. McMillanThe downtrend on the $SPX chart is obvious, even to the casual observer. Not only are there now lower highs and lower lows, but the short-term moving averages as well as the "...

Mar, 16, 2026

By Lawrence G. McMillanOver the years, we have discussed a lot of volatility-based trades. Since volatility is high now, a number of them are apropos, so for newer and older subscribers alike, this...

Mar, 16, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on March 16, 2026.

Mar, 13, 2026

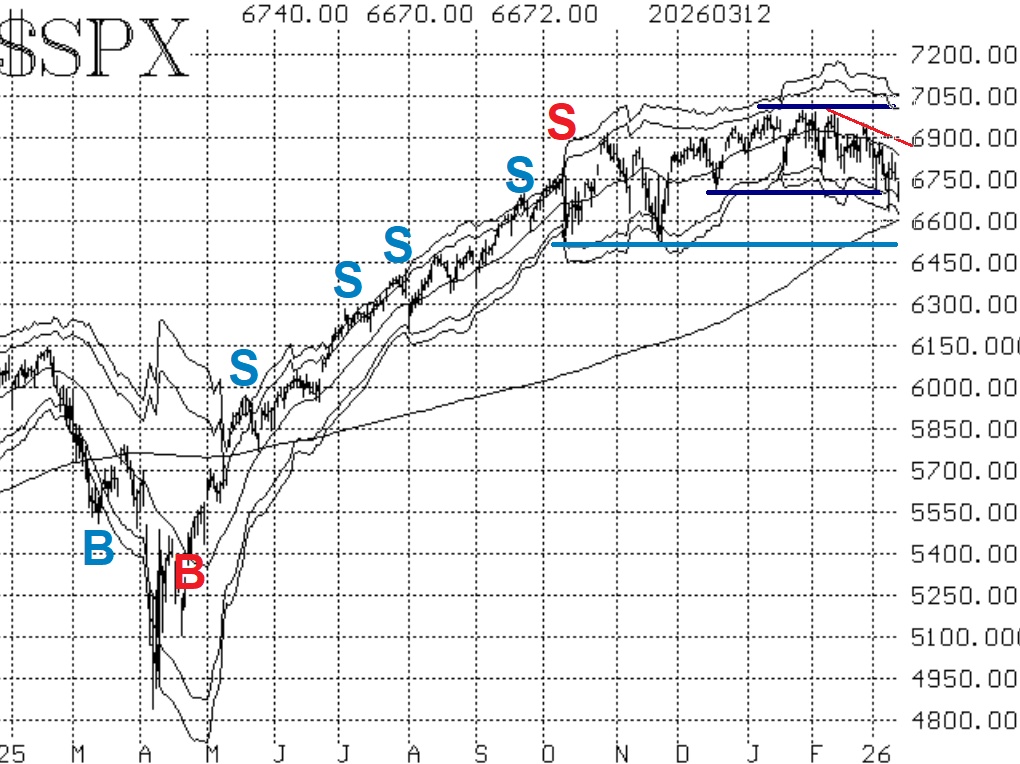

By Lawrence G. McMillanIt certainly took a while, but $SPX has finally closed below its December low of 6720. On average, statistics show a further decline of 10% when that occurs. Sometimes these...

Mar, 11, 2026

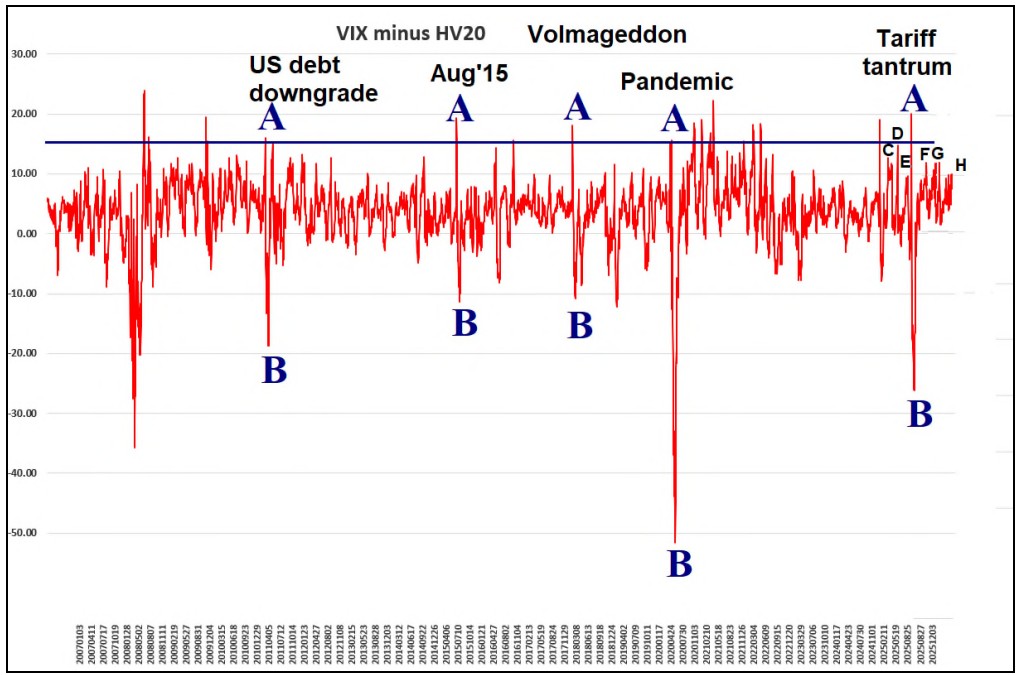

By Lawrence G. McMillanVolatility and the stock market normally move in opposite directions. But occasionally, the relationship between $VIX, $VIX futures, and the S&P 500 becomes distorted.When...

Mar, 09, 2026

By Lawrence G. McMillanBoth in May 2025 and October 2025, we published articles with the above title. I won’t include them here, because they were too long, but one can find them in the...

Mar, 09, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on March 9, 2026.

Mar, 06, 2026

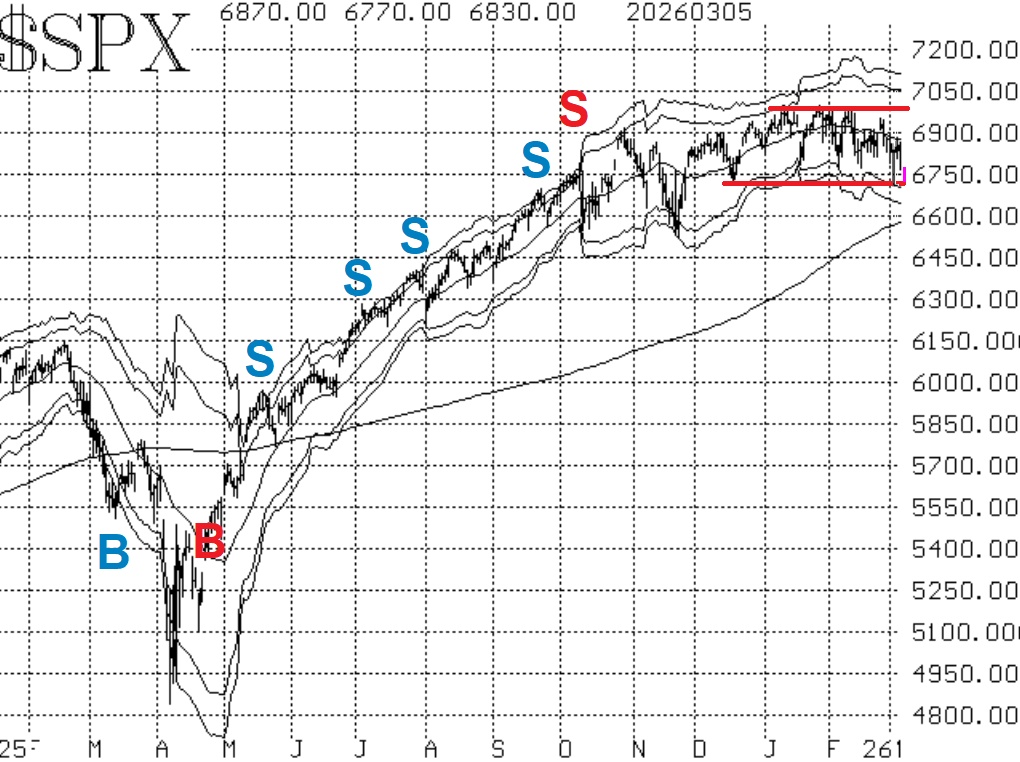

By Lawrence G. McMillanThe bulls are fiercely defending the 6720 area, which is the lower end of the trading range and is also the December low. The bottom line is that swing traders who are buying...

Mar, 05, 2026

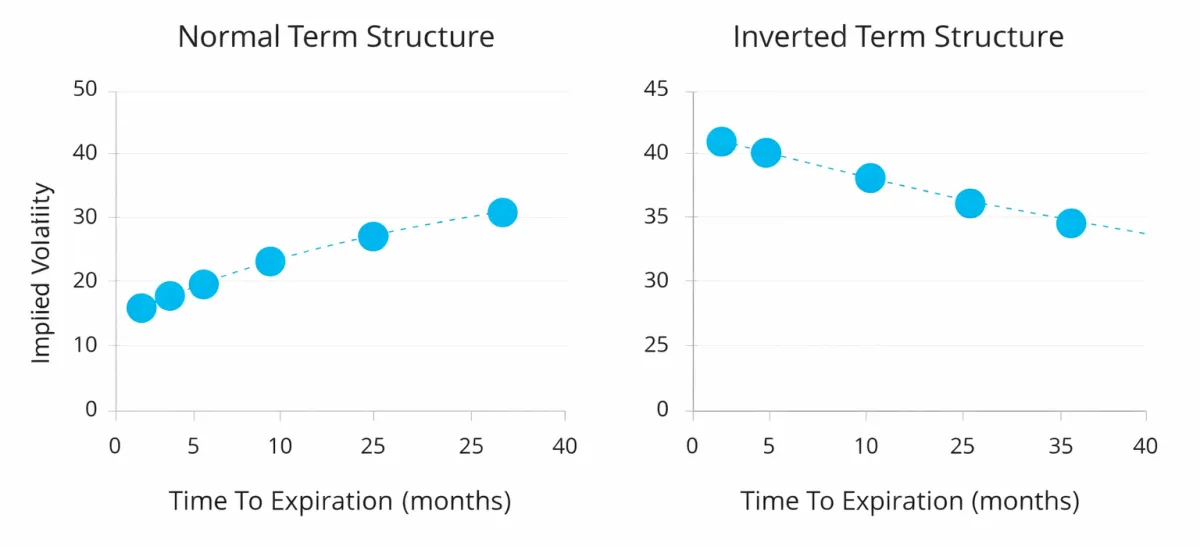

By Lawrence G. McMillanPredicting stock prices consistently is difficult.Predicting volatility behavior, however, is often easier.That is why many professional option traders focus more on volatility...

Pages

© 2023 The Option Strategist | McMillan Analysis Corporation