Jun, 12, 2026

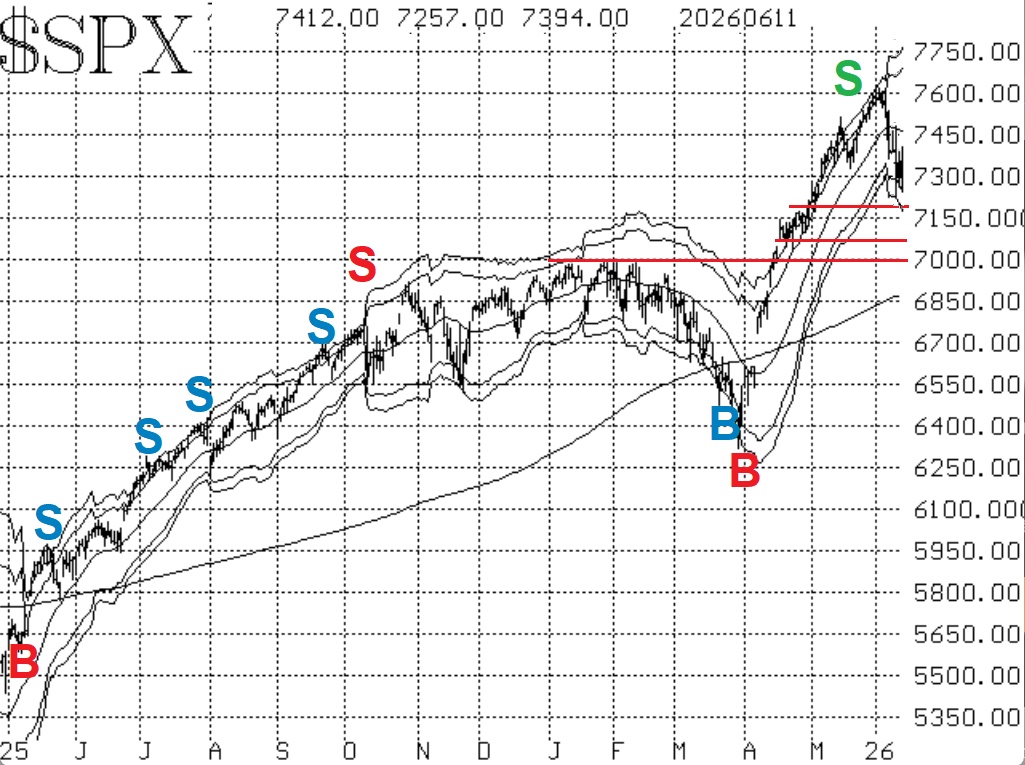

By Lawrence G. McMillanIn all, the correction from the early June highs to the lows of this week was about 5%. That was enough to at least temporarily remove the "bullish" designation from the $SPX...

Jun, 08, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on June 8, 2026.

Jun, 05, 2026

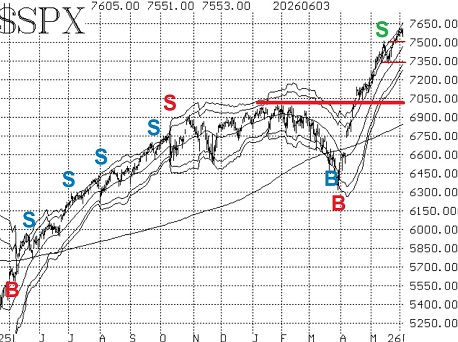

By Lawrence G. McMillanThe S&P 500 Index ($SPX) has advanced on ten of the last eleven trading days. Needless to say, the Index chart has strong upward momentum. Media articles continue to focus...

Jun, 01, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on June 1, 2026.

May, 29, 2026

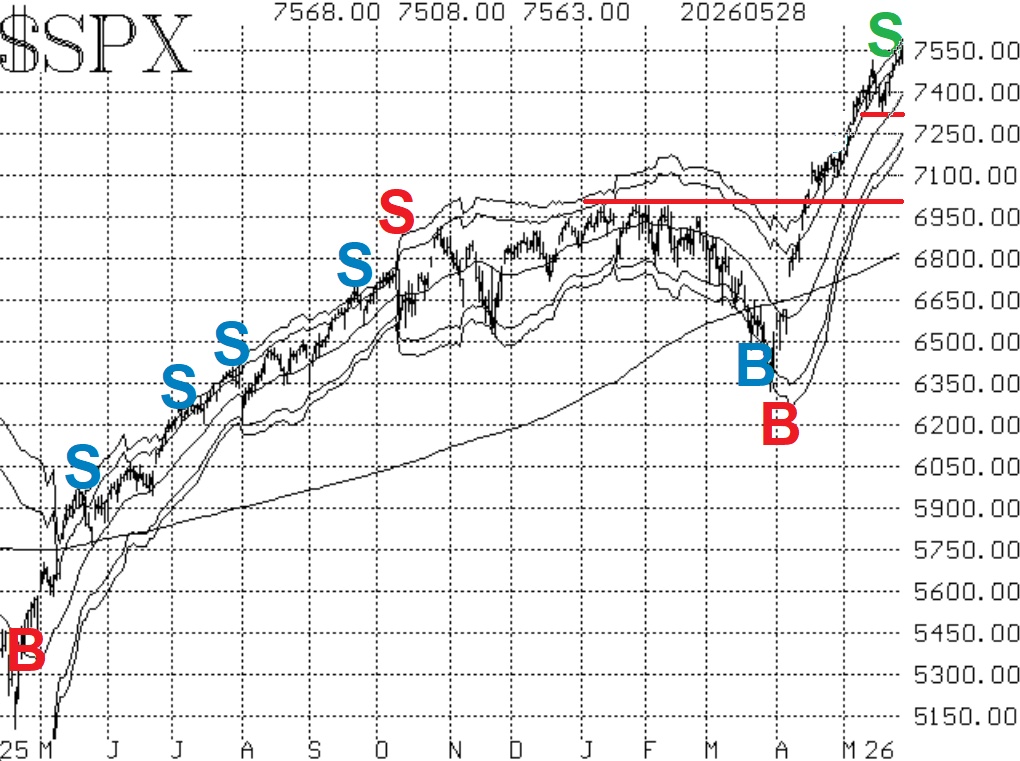

By Lawrence G. McMillanThis market is the epitome of our phrase, "overbought does not mean sell." It just keeps going higher, and now the rally has broadened enough so that the Dow ($DJX; DIA),...

May, 29, 2026

By Lawrence G. McMillanIn 1973, inflation, interest rates, and impeachment dominated headlines during a brutal bear market. Today, a different set of "I's" is making news, yet stocks continue to push...

May, 28, 2026

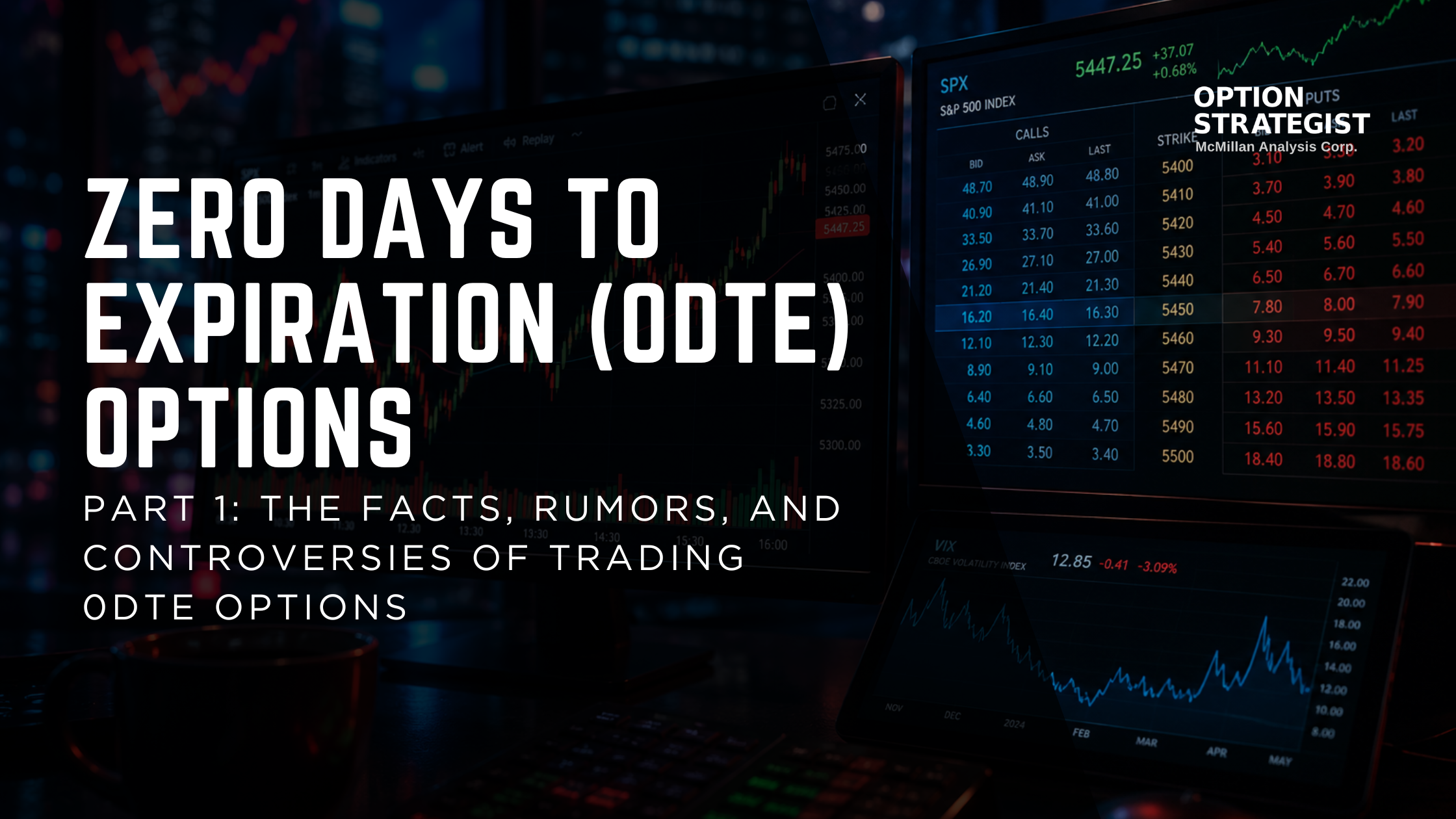

By Lawrence G. McMillan0DTE (Zero Days to Expiration) options have rapidly become one of the fastest-growing areas of the options market. Trading volume in products such as $SPX, SPY, and QQQ has...

May, 26, 2026

By Lawrence G. McMillanJoin Larry McMillan as he discusses the current state of the stock market on May 26, 2026.

May, 22, 2026

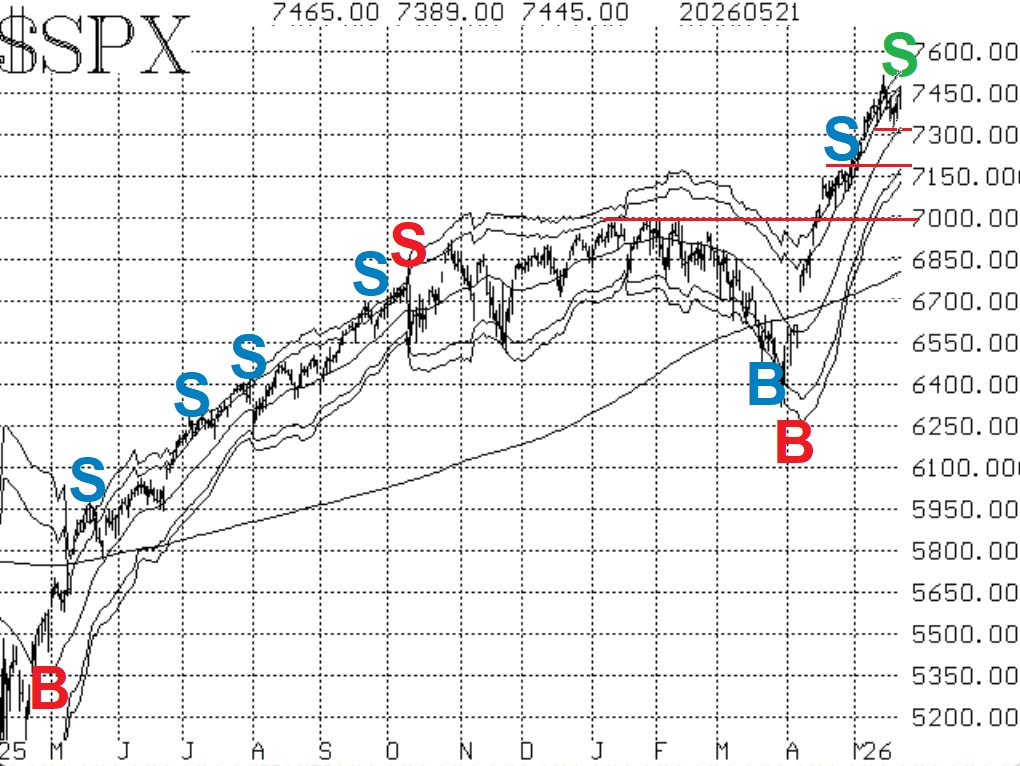

By Lawrence G. McMillanThree different internal indicators have generated sell signals over the past week or so, but the most important indicator -- the chart of $SPX remains bullish. When these...

May, 20, 2026

By Lawrence G. McMillanThis Memorial Day weekend, McMillan Analysis is offering 25% off all advisory services.Whether you’re looking for daily market commentary, volatility analysis, put-writing...

Pages

© 2023 The Option Strategist | McMillan Analysis Corporation