By Lawrence G. McMillan

This week, the OCC sent out a notification that VMIN was going to split 2-for-1. Because the symbol seemed like something related to volatility, I checked into it. What I found was an ETF that looked potentially interesting, and that had been listed last May. For some reason, I had never heard of it, so I decided to check it out.

Background

One cannot trade $VIX directly because of the way it is constructed. So, many innovative (and some, not so innovative) firms have tried to come up with products that simulate the movements in $VIX. We have written about many of them. The original one – VXX – was introduced by Barclay’s Bank in January 2009. For the first time, institutions that otherwise could not trade futures could hedge volatility by going long VXX. That has led to its popularity, as it currently trades about 30 million shares a day. Unfortunately, the performance of VXX is a real dog. It underperforms $VIX most of the time – whenever the term structure of the $VIX futures slopes upward, as it does in all but the most bearish markets. However, in a bear market, when $VIX explodes and the term structure of the $VIX futures inverts, VXX does outperform $VIX. Hence it is useful in those situations.

VXX is an Exchange Traded Note (ETN), as opposed to an ETF, which means that it is really a debt of the issuing bank (Barclay’s in this case) if one were forced to try to redeem the notes. That is a credit risk that is minuscule most of the time, but could be a problem in a severe bear market – just when you would need VXX the most – if Barclay’s were to go out of business. Since we saw some large banks fail in the last financial crisis – Bear Stearns and Lehman Brothers – it is not impossible that this risk could materialize. Even so, most traders who want this protection are willing to accept that (currently extremely small) risk.

Since VXX was popular, many copycat ETN’s and even an ETF or two, followed quickly. One of the most popular was XIV ($VIX spelled backwards), which is the negative of $VIX. XIV trades about 12 million shares per day. For the most part, XIV performs opposite to VXX. So when the term structure of the $VIX futures is sloping upwards, as it usually is, that is a boon to XIV. One of the most popular hedge fund strategies since $VIX futures were listed in 2004 is to short those futures a few months out and let the time decay bring them down in price to $VIX. That is a strategy that most individuals cannot employ, for reasons of capital and/or being able to sleep at night. But the same “time decay” that affects the $VIX futures is what makes VXX decline in price as well. Likewise it is what propels XIV upward. So the average investor learned that buying XIV was a viable strategy until the market takes a nasty downturn. So those traders attempt to exit their XIV positions during those bearish market periods, thus leaving them to profit in most other markets.

Both XIV and VXX employ, as their underlyings, the two front month $VIX futures. It is well known that the shorter the time duration of any product attempting to simulate the movements of $VIX, the better the correlation. As a result, the CBOE introduced $VIX weekly futures some time ago, and later introduced weekly options on $VIX (whose underlyings are those weekly $VIX futures). These shorter-term products theoretically give one the opportunity to simulate $VIX better. To my way of thinking, these are best used from the long side as disaster protection for one’s portfolio.

VMIN

Evidently there is a demand for a “short $VIX” product that does even better than XIV. Thus we come to VMIN, an ETF (by way of using a holding company to hold the actual underlying instruments that VMIN buys) that simulates “short $VIX” more directly. VMIN was created by VolMAXX, the brand name of volatility related ETF’s sponsored by REX shares. REX is a sponsor of a broad range of ETFs.

VMIN is not very popular. I think they have done a terrible job of marketing themselves, considering that we try to read whatever we can about volatility derivatives and had never heard of it until now. It trades less than 10,000 shares per day on most days.

VMIN attempts to shorten the overall average holding periods by combining $VIX derivatives in order to simulate the (opposite) movement in $VIX, but still capture some of the “time decay” that these derivative products have built into them most of the time. In the prospectus, it states that the VMIN intends to maintain a weighted average time to expiration of less than one month at all times.

At first, I thought VMIN would just use a XIV-like structure of two $VIX futures, but with shorter durations. However, they have a different approach than that. There is full information available on their web site, at http://www.volmaxx.com/rex-volmaxx-short-vix-weekly-futures-strategy-etf.

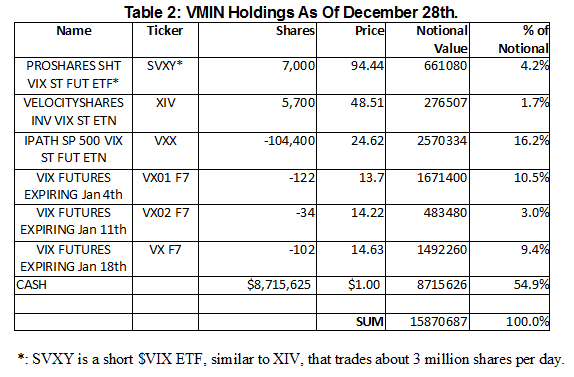

Their holdings are available on their web site. This is a snapshot of their holdings on December 28th:

I found this portfolio to be odd, in light of the stated objectives. It might seem strange that 54.9% is in cash. But in the VMIN documents, it is stated that the “notional value of the short VIX [products] would be approximately equal to the Fund assets at the close of each trading day.” In other words, computing it the way that’s shown in Table 2, the cash position would be about 50% – equal to the notional value of the various $VIX products.

Every holding in Table 2 is a “short $VIX” holding, since SVXY and XIV are inverse VIX products, and the others are short positions of long volatility products. So these are in line with the stated VMIN objectives.

But, note the large position in short VXX, accompanied by smaller positions in SVXY and XIV. These use the “old-fashioned” time frames, which I thought VMIN was trying to shorten. These have a time to expiration of one month. So the only products that shorten the time frame are the three positions in VIX futures. Collectively, these make up about 23% of the portfolio in Table 2 (or 51% of the non-cash portfolio).

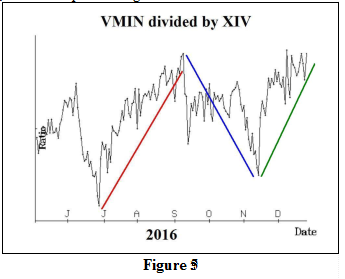

There is not a long historical time frame for comparison, but I wanted to compare how VMIN has done in comparison to XIV. Figures 5 and 6 depict this. The time frame covers the entire trading history of VMIN. In figure 5, the graph shows VMIN divided by XIV. When the graph is rising (red line and green line), VMIN is outperforming XIV; when the graph is falling (blue line), XIV is outperforming VMIN.

There is not a long historical time frame for comparison, but I wanted to compare how VMIN has done in comparison to XIV. Figures 5 and 6 depict this. The time frame covers the entire trading history of VMIN. In figure 5, the graph shows VMIN divided by XIV. When the graph is rising (red line and green line), VMIN is outperforming XIV; when the graph is falling (blue line), XIV is outperforming VMIN.

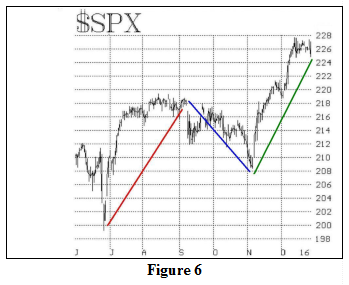

Figure 6 is the graph of $SPX over this time frame and is more or less aligned directly below that of Figure 5, so that one can directly compare how the outperformance of VMIN lines up with the performance of the stock market. It is easy to see how the various colored lines match with each other. Throughout July, the post-Brexit rally was taking place, and $VIX was dropping, so the inverse $VIX products did well. VMIN did better than $VIX, as noted by the red line. But then $SPX flattened out in August, yet the term structure of the $VIX futures continued to slope steeply upward. When that happens, the inverse $VIX products do well also, and VMIN continued to outperform XIV over that time frame as well.

The out performance of VMIN ended when the market went into a pre-election decline through September and October. During that time, both VMIN and XIV struggled, but XIV did better than VMIN.

VMIN resumed its dominance, post-election, as it has outperformed XIV over the past two months.

So VMIN is a bit like XIV on steroids. Shortening the “time to expiration” will do that. If that’s what you’re looking for, it may be the better product to use, modulo the illiquidity.

In theory, VMIN has listed options and XIV does not, but it looks to me like the VMIN administrators twisted someone’s arm to get them listed. There is literally no open interest and the markets are ridiculously wide. So, for all practical purposes, VMIN does not have listed options.

In summary, when one looks “under the hood,” VMIN doesn’t seem quite so interesting – mainly because of its lack of liquidity. But for those traders who have discovered that XIV goes up most of the time and are thus maintaining a long position, VMIN could prove to be a reasonable alternative if one wants more leverage to the strategy of being short $VIX and being short the time premium in its derivatives.

© 2023 The Option Strategist | McMillan Analysis Corporation