By Lawrence G. McMillan

One doesn’t often consider butterfly spreads or condors, say, as short-term speculative strategies. However, they can be, if you set them up that way. The main problem with butterflies, in particular, is that they don’t reach their profit potential until very near expiration (unless the strikes are extremely far apart).

Typically a butterfly spread is constructed in this manner:

Example:

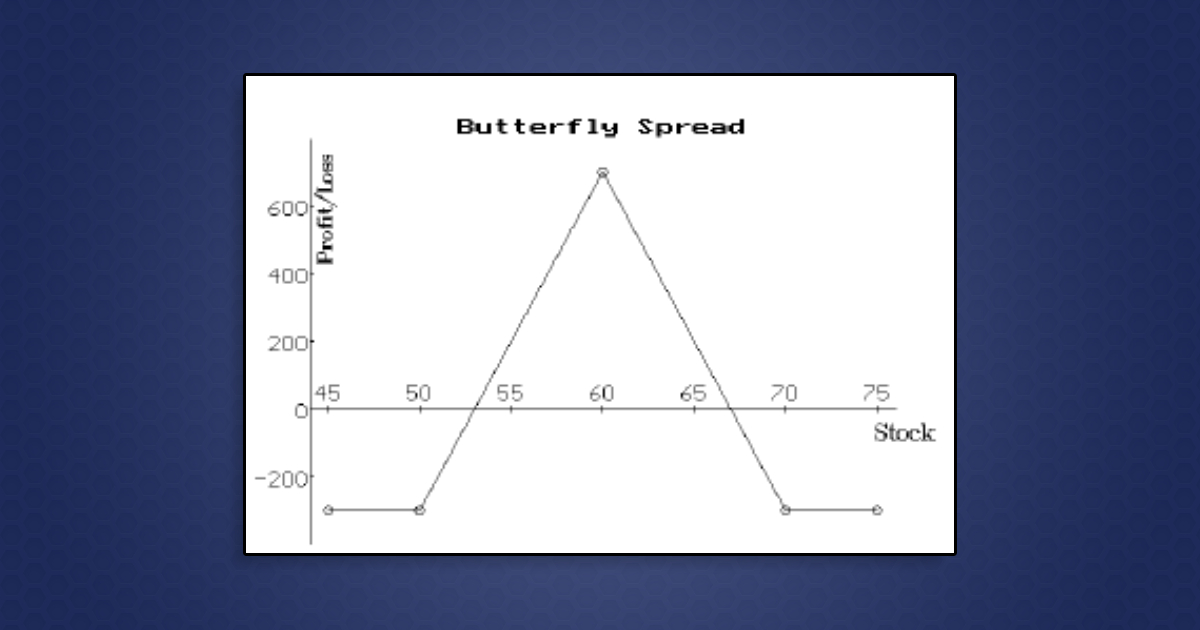

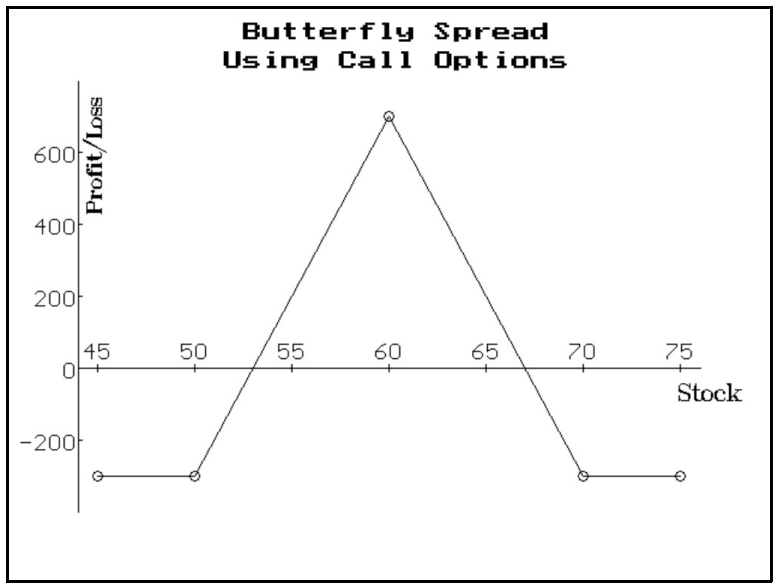

Buy 1 XYZ May 50 call @ 6

Sell 2 XYZ May 60 calls @ 2

Buy 1 XYZ May 70 call @ 1

Net debit : 3 points, or $300

The spread has limited loss and limited profit. The maximum loss is equal to the initial debit of $300 paid for the spread. The maximum loss would be incurred if XYZ were below 50 or above 70 at expiration. The maximum profit occurs at the middle strike at expiration, and in this case is equal to $700. The position is shown graphically below.

The collateral margin required for a butterfly spread is the maximum loss. In some cases, brokerage firms may want more margin. If that is the case, change firms. There is no reason that the clearing firm should be asking for more margin than the maximum loss.

A butterfly spread can also be established with put options – something like this...

Read the full article by subscribing to The Option Strategist Newsletter now. Existing subscribers can access the article here.

© 2023 The Option Strategist | McMillan Analysis Corporation