By Lawrence G. McMillan

We have written many times about the “Big (Volatility) Short.” It is a very profitable trade, for the most part. It comes about because of the upward-sloping term structure of the $VIX futures during a “normal,” bullish market. In its simplest, original form, one merely shorts the $VIX futures a month or two out in time and sits back, waiting for the passage of time to bring the futures prices down to meet $VIX at expiration. In effect, the “time decay” of the premium in the $VIX futures produces a profit for the short sellers of $VIX futures.

The strategy only loses money if $VIX rallies sharply and/or if the $VIX futures trade at a discount to $VIX, in which case time decay is negative (i.e., the futures rise to meet $VIX at expiration). Both of those things tend to happen simultaneously in a bearish stock market.

From the inception of $VIX futures trading in 2003 to early 2009, this was the only way to trade “the Big (Volatility) Short.” In fact, the market itself halted the practice of this trade, with the huge spike in volatility in 2008. Most practitioners of the strategy were wiped out or suffered large losses at that time.

Then, in early 2009, Barclays introduced the first Volatility ETN, called VXX. VXX is really just a blend of the two front futures months, so shorting VXX is the equivalent of shorting the $VIX futures. Since VXX was fairly liquid and popular, it was available to borrow and short.

Shortly after VXX gained popularity and liquidity, the “inverse Volatility ETN” arose, called XIV. It behaves in pretty much exactly the opposite way to VXX. So a long position in XIV is akin to a short position in VXX. This opened up the “Big (Volatility) Short” to everyone, for even the smallest investor could buy shares of XIV. There was no need to go through the hassle of borrowing shares of VXX to short.

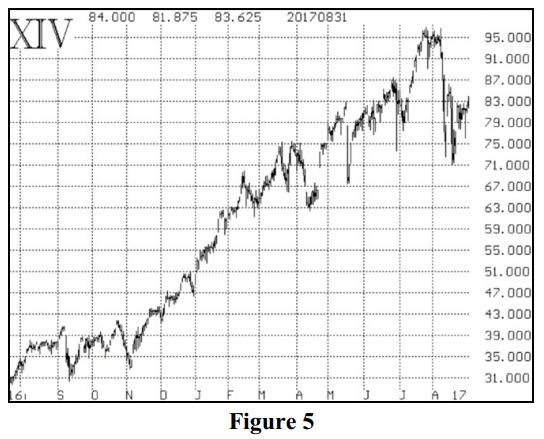

Owning XIV is the epitome of this phenomenon of shorting volatility. Its chart has not been so healthy lately, though (see Figure 5, but most players in this space couldn’t care less about the chart – they’re only concerned with an upward-sloping $VIX futures term structure, and that they have. You can see the strong upward move in XIV from last November, and that is what has fanned the flames of what can only be described as a “short volatility” frenzy. Eventually, this will end badly, of course, but it’s hard to predict how or when.

So many articles have been and are being written on the subject that it’s hard to follow them all. One caught my eye recently, though as a practitioner of the “short volatility” strategy postulated that it takes advantage of a market inefficiency, and postulated that the inefficiency would eventually disappear.

The author identified the inefficiency as the upward slope in the term structure of the $VIX futures. He predicted it would eventually go away, and then the trade would end. Well, he’s right about one thing: if the term structure is flat, shorting VXX or being long XIV doesn’t have any “edge.” It would simply become a volatility trade, profiting or losing money only on the basis of movement in $VIX. There would essentially be no “time decay” in the $VIX futures, and hence no “free money” for those who are shorting volatility futures.

But will the $VIX futures term structure ever flatten? I don’t think so. We have written in the past about what causes the term structure to slope upward in a bullish stock market. Here’s a quick summary:

Suppose near-term volatility is relatively low, as is generally the case in a bull market. Further, suppose that a trader comes to a market maker and says, “What implied volatility will you charge me for a call option that is due to expire in just a couple of weeks?” No one knows where volatility is going to be in two weeks, but odds are that it will be pretty close to where it is now, so the market maker will generally price the option with an implied volatility only slightly higher than the current volatility, or the current $VIX.

Then suppose the same option buyer asks the market maker to price a 3-year option. We know that no one knows where volatility is going to be in three years, so the market maker would generally be leery of pricing it too low, so he will use something close to, or maybe even slightly above, the long-term average volatility of the underlying. In this case, suppose the buyer is looking to buy a 3-year call on SPY or $SPX. The market maker is probably going to charge something like a 22% implied volatility for that call, because that is the longer-term volatility of the index.

So this means that a short-term $VIX futures will be priced just slightly above the current price of $VIX, while a long-term 3-year $VIX futures contract (if one existed) would be priced at 22. For expirations in between, the slope is somewhat linear between the lower-priced short-term futures contract and the longer-term one. Hence the term structure of the $VIX futures slopes upward. That is not going to change, unless market makers are willing to sell long-term calls for a very low volatility – a virtually impossibility. Hence, in a bull market, the term structure is going to slope upwards. It’s just a fact of life.

In recent years, both realized and implied volatilities have become quite depressed, as this long-term bull market rolls along. This new generation of “short volatility’ traders thinks that this is the new norm. But just as the low volatilities of 1993 and 2006 seemed permanent, they eventually gave way to massive increases in volatility, and so will this market – eventually. Another popular way of being short volatility is via SVXY, which is an ETF, not an ETN.

Is a long bear market the only thing that could kibosh the short volatility trade? No, there are some structural inefficiencies in the markets that could be a problem. Very few traders know what will happen to XIV if $VIX futures explode to the upside. One has to read the Prospectus to see what will happen, and most owners of XIV have not and most likely will not do so. The worry is that if $VIX futures were to more than double in a day, then XIV and SVXY would be worth less than zero!

The underwriter (think “market maker”), which happens to be Credit Suisse (CS) for XIV, doesn’t want that to happen, of course, because CS would be on the hook for any losses if the value of XIV dropped below 0. So, in the case of XIV, if the futures gain 80% on a given day, the underwriter will begin to liquidate XIV – hoping to cover all the short futures before they rise by more than 100% on the day. That will eventually wipe out XIV at nearly a total loss to holders. The underwriter then has the right to accelerate the expiration of the ETN, and holders will receive a cash payout for whatever is left (if anything). In that case, the ETN will cease to trade any longer. Of course, this presupposes that the short $VIX futures can even be covered. One would have to expect it would be difficult, because if they’ve already risen 80% without the underwriter in there buying back his shorts, they will really take off if the short covering accelerates in earnest.

As for SVXY, I spoke with the ProShares people (the underwriter) and was assured that the investor cannot lose more than 100% of his investment, regardless of what happens to the actual short futures contracts. In practice, if the value of SVXY at the end of the day is less than or equal to zero, it would cease to exist. Even if the investor cannot lose more than 100%, Proshares can, and Proshares certainly would not want unlimited losses in the short futures, so they would be madly covering them as well – accelerating the futures ascent just as Credit Suisse would.

The combined actions would be quite startling and would certainly have after-shocks in other parts of the market. Having traded through the Crash of ‘87, one learns not to discount things like this. In theory, $VIX rose from about 30 to 150 on the day of the Crash, so it is certainly possible for a double of $VIX futures to occur in a single day.

Note that this dire scenario would not unfold if, for example, $VIX futures were to rise 50% one day and then 50% again the next day. That would certainly be very harmful to the value of XIV and SVXY, but it would not cause the buying panic in the $VIX futures described above. However, with massive redemptions (selling) of the XIV and SVXY shares by holders of those ETFs and ETNs, there could be massive buying of $VIX futures anyway – perhaps in a more orderly manner – as the underwriters unwound the futures positions to match the redemptions in the shares.

The bottom line is that the Big (Volatility) Short is an excellent trade that takes advantage of an upward sloping term structure in the $VIX futures. If that term structure, however, flattens or begins to slope downward, bad things happen to the Big (Volatility) Short trade. The rapidity with which the term structure makes that change will have a lot to do with just how bad the losses are that are incurred by the volatility shorts. Most smart players – hedge funds, family offices, etc. – are quite leery of the short volatility trading strategy right now, because of the extremely low levels of $VIX and because it’s such a crowded trade. However, it seems that “everyone” is warning against the trade right now, so it will probably continue to work for quite some time before – unexpectedly – a problem explodes on the scene.

In the articles we previously have written about the Big (Volatility) Short trade, we had exits in mind. Those should be paramount for anyone using this strategy. Simplistically, if the term structure flattens, get out of XIV and SVXY until it steepens again. There is no advantage to being in those securities when the $VIX futures term structure is flat or sloping downwards. The term structure will flatten before disaster occurs.

This article was originally published in the 9/1/17 edition of The Option Strategist Newsletter.

1Technically, it can be demonstrated that a short position in VXX slightly outperforms a long position in XIV, but the difference in performance is usually small and thus is of little concern for most traders who trade XIV from the long side.

2An ETF (Exchange Traded Fund) holds the underlying securities in “trust,” so that in event of a default of the underwriter, the underlying securities could be distributed to shareholders – thereby maintaining the shareholder’s value. An ETN (Exchanged Traded Note) on the other hand, is just a debt obligation of the underwriter. So if Barclays fails, for example, holders of VXX will have to stand in line with other creditors of Barclays to recover cents on the dollar for their VXX shares. This theoretically makes ETF’s more desirable than ETN’s, but in reality the chances of these major underwriters going bankrupt is deemed to be negligible, so XIV and SVXY trade for the same relative price.

© 2023 The Option Strategist | McMillan Analysis Corporation