Optionstrategist.com

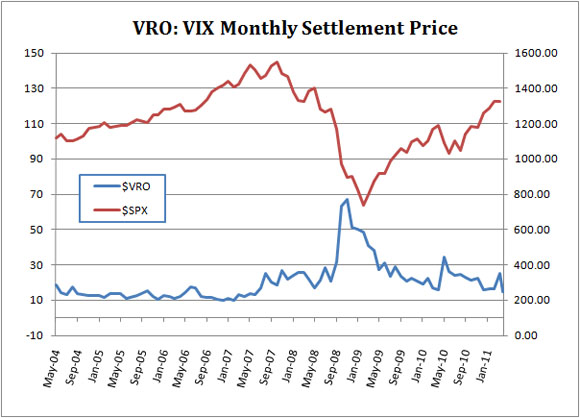

The June VIX Futures settled at 19.73 this morning ($VRO), up $1.71 from the May expiration. This month's settlement is the 2nd highest this year and is the 2nd consecutive higher settlement off the low April bottom.

For an extenisve analysis of the Volatility and Variance Futures and Options Markets, subscribe to The Option Strategist Newsletter.

By Lawrence G. McMillan

$VIX spiked up to almost 20 last Friday and then reversed back downward to nearly 17. Currently, it stands at 17.82. A spike peak reversal of that magnitude is at least a short-term buy signal for the stock market. $VIX has probed to or above the 19 level four previous times since mid-April, and a tradable stock market rally has followed each time. Will this be the case again this time, considering that there are other, more negative, indicators at work as well?

By Lawrence G. McMillan

Breadth was terrible yesterday, making Wednesday a true 90% down day in terms of “stocks only” data and a 90% down volume day in NYSE terms. This is the first true 90% down day since March 10th. That usually means that one can expect a reflex rally in the next day or two, but also indicates that lower prices eventually lie ahead.

VIX Edging Higher: A Warning?

By Lawrence G. McMillan

The settlement for the CBOE Volatility Index (VIX) May futures contract was 18.02, up by a healthy percentage from the April settlement of 14.86. Moreover, VIX itself began to rise late this week. A rising VIX is generally symptomatic of a bearish stock market, so these rises may be a warning sign to stock holders that a correction is approaching.

This morning, the $VIX April futures settled at 14.86, the lowest futures expiration since June of 2007 which was near the end of the last bull market. The $VIX index also opened this morning at a recent low of 14.31. Even though this might be considered overbought, with $VIX trending lower the market remains bullish.

Trading has begun on the CBOE Futures Exchange (CFE) in Gold Volatility futures. If you’ll recall, a VIX-like calculation can be made on any set of option prices on an individual stock, as long as there are continuous markets being made in the options.

The CBOE has been publishing a “Gold VIX” under the symbol $GVZ for some time. This calculation is based on the options on the Gold ETF (GLD).

Now, futures have begun to trade on $GVZ. Their base symbol is GV, and there are futures in the May, June, July, Aug, and Sept at this point.

Several new volatility products have recently entered the market or will soon be listed for trading. The most promising of these is the new set of contracts to be listed on the Chicago Board Options Exchange. Trading began on March 25 in Gold Volatility Index futures on the CBOE. Options on them will be listed on April 12. Many other new products will follow in due course.