By Lawrence G. McMillan

In a move which some might call a “day late and a dollar short,” there are now going to be some products via which European volatility can be traded in the U.S. markets. There have long been volatility futures on the “European $VIX” – VSTOXX. VSTOXX measures the implied volatility of the European EURO STOXX 50 Index, using the same methodology that $VIX does.

Janus has listed two ETN’s which are volatility ETN’s on the VSTOXX. EVIX is the forward (normal) Volatility Index, and EXIV is the reverse. These are akin to VXX and XIV, respectively. At this time, there is no “double $VSTOXX” ETN listed in the U.S. (i.e., nothing akin to TVIX or UVXY).

U. S. Indices European Counterpart

$SPX Euro STOXX 50 Index (trade only in Europe)

$VIX $VSTOXX (trade only in Europe)

VIX Futures VSTOXX futures (trade only in Europe)

VXX EVIX

XIV EXIV

Furthermore, the CBOE has listed options on EVIX. Does this mean that there won’t be options on EXIV (the reverse volatility index), just as there aren’t any options on XIV? I guess so.

If one looks “under the hood,” EVIX and EXIV are constructed in a similar manner to VXX and XIV – using the underlying futures. In the case of EVIX and EXIV, they use the VSTOXX mini futures that trade in Europe (they are apparently called “mini” because they are 100 Euros per point, as opposed to $1,000 per point for U.S. volatility futures). As we know, when the term structure of the futures slopes upward, that is a detriment to EVIX and a boon to EXIV. But in a bearish environment, when the term structure of the futures slopes downward, the reverse occurs: EVIX will benefit, and EXIV will suffer. So, in short, they will have the same biases that VXX and XIV do.

VSTOXX futures trade in a very similar manner to VIX futures. Here is the current term structure:

VSTOXX Futures Month Price

May 15.10

June 16.20

July 17.20

Aug 17.95

Sept 19.00

If you are looking for a cheap way to see VSTOXX futures quotes, I found them here:

http://www.eurexchange.com/exchange-en/products/vol/vstoxx/vstoxx--futur...

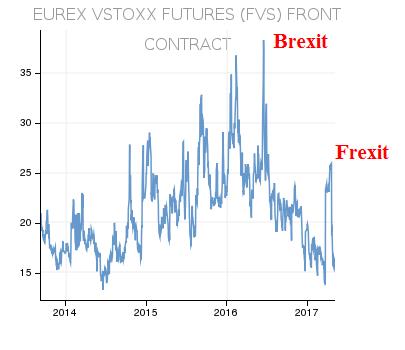

The reason I say this is a “day late and a dollar short” is that all of the interesting action of “Frexit” (and “Brexit,” too, for that matter) has already taken place (chart, right). Now, European volatility is back in line with U.S. volatility in a rather boring state. Nevertheless, these new products may give us some additional opportunities for our “usual” volatility trading strategies.

For further information, one might want to read:

https://www.etftrends.com/2017/05/the-first-european-volatility-etns

http://ir.cboe.com/press-releases/2017/05-04-2017-181851569.aspx

http://ir.cboe.com/press-releases/2017/05-03-2017.aspx

This article was featured in the 5/5/17 edition of The Option Strategist Newsletter.

© 2023 The Option Strategist | McMillan Analysis Corporation