By Lawrence G. McMillan

Recently, the CBOE’s Volatility Index ($VXST) closed above all three of the other CBOE Volatility Indices. At the time, it struck me as being a rather rare occurrence, and it seemed there might be some considerations as to forthcoming market movement. Consequently, a rather extensive study was performed, and indeed a trading system did emerge, as this article will reveal.

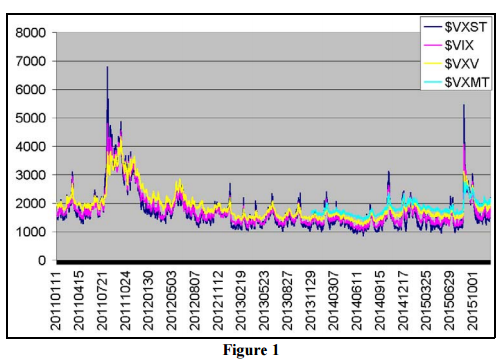

Previously we had identified a “$VIX Crossover” trading system., and so it was logical to try to incorporate some of the facts of that system into this new system. Even so, there were several variations of the system that needed to be analyzed. We can’t just buy “the market” every time $VXST closes above the other three Volatility Indices, for – upon inspection – the condition is not all that rare: $VXST has closed above all three other Volatility Indices on 161 of the last 1253 days – or about 13% of the time. They tend to come in bunches, however – occurring when there is panic in the option market, when there is heavy demand for near-term options. Figure 1 shows all four indices going back to November, 2011, which is when the $VXST Index was created.

$VXST is the dark blue line. You can see that it pokes up above the other relatively infrequently – only about 15 times since the beginning of 2012. However, as we noted earlier, it can stay above all the others for several days at a time when it does rise above them.

You will also notice the aqua line that starts in December, 2013. That is when the $VXMT – the longest-term of the CBOE Volatility Indices – was created. So, prior to that on the chart, $VXST only had to rise above the other two indices in order to be the highest. Since the creation of $VXMT, it had to exceed three others.

The “$VIX Crossover” System

The “$VIX Crossover” system looks only at the relationship of $VIX and the next-longest-term CBOE Volatility Index, $VXV. That system is simple enough: when $VIX closes above $VXV, one is “on alert” for a broad market buy signal. And when $VIX closes back below $VXV, that is the buy signal itself. Buy signals from this system seem to be powerful, but mostly in the short-term. Their best gains come in the first trading days after the buy signal is issued.

The New System

Many of our trading systems generate signals by:

1) determining when the market is extremely oversold,

and 2) waiting until the oversold condition abates and then buying.

We will use a similar strategy here. The market is considered “oversold” when $VXST is the highest of all of the CBOE Volatility Indices. We will look to buy “the market” when it is no longer the highest index. It would be too onerous to require $VXST to fall back below all of the other indices before we buy; we would miss a lot of the market’s rise if the condition were that restrictive.

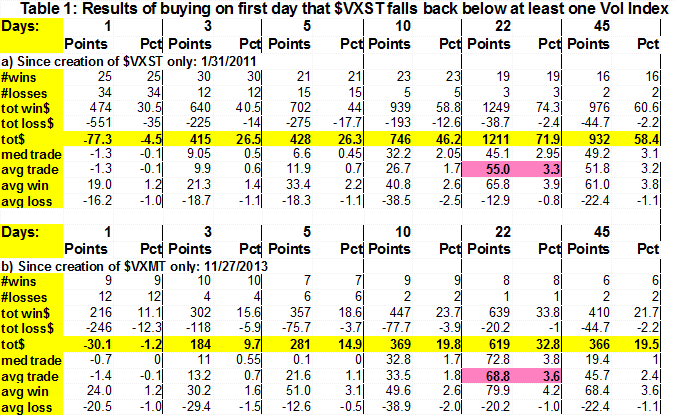

All of the results in this article will show a) the results back to November, 2011 – when $VXST was first created – and b) back to December 2013 only, when $VXMT was created. Obviously there are fewer data points under condition b), but it is the one that will be in force going forward. In all cases, we will measure the results of buying the $SPX Index and holding for 1, 3, 5, 10, 22, and 45 trading days after the signal. Any buy signal would be stopped out if $VXST once again rises back above all of the other indices, regardless of the time period that has elapsed since the buy signal.

Table 1 shows the results of this system. Note that the longer-term holding periods show fewer trades than the short-term ones. That is due to the trade being stopped out by $VXST once again rising above all the other indices. Table 1 is divided into two parts – the top part encompassing part a) as noted above (back to 2011) and the bottom part encompassing part b) (back to 2013).

There is quite a bit of information in the table. Let’s start with the Total Points (in $SPX terms) or Total Percent gained or lost. Those are the rows highlighted in yellow. Notice that the system is profitable for both time periods (a or b), for all holding periods (3, 5, 10, 22, and 45) except the one-day holding period.

The one-day holding period is a problem because quite a few times, $VXST would fall below some of the other indices (thereby triggering the buy signal) only to rise right back above the next day. Note that there were 59 one-day holding periods (25 wins and 34 losses – see the upper left corner of Table 1). But there were only 42 holding periods of three days. That means 17 of the original 59 trades were stopped out on Day 1 (Day 2 stops are included in the 3-day results). More about that in a minute.

The sample sizes are rather small, but at this point it seems that the best exit point is 22 days, if you can make it that far. Those are the cells highlighted in pink. For study a), the results are only marginally better than the 45-day holding period, but for study b), they are quite a bit better at 22 days. All this means is that if we are in a trade and have managed to stay in the trade for 22 days without being stopped out, we should consider exiting – or at least taking a major portion of the position off.

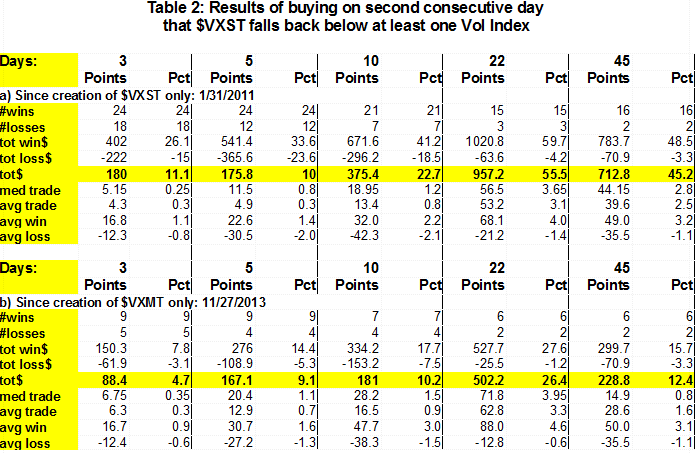

Now, back to the one-day holding period problem. We don’t know when we start out if we’re going to be able to survive past the one-day holding period or not. But what if we didn’t enter the buy signal until there were at least two consecutive days when $VXST remained below at least one index? In other words, everything else would be the same as the system laid out above, but now after a period of days when $VXST was higher than all of the other Volatility Indices, we would only generate a buy signal if it closed below at least one of the other Vol Indices for two consecutive days.

The results of this approach are shown in Table 2. To make a better comparison between Table 1 and Table 2, Table 2 only contains five columns: 3-, 5-, 10-, 22-, and 45-day holding periods that match exactly with those of Table 1 as far as their end points are distant from the original buy date of Table 1.

The results on Table 2 are generally better – mainly because we avoid those first-day losses. The “3-day” results in Table 2 encompass getting stopped out on Day 2 or Day 3, but bypasses the Day 1 negativity that was shown in Table 1. These “3-day” results in Table 2 are positive.

Of course, some of the first days were big up days, and we miss those, too, with this approach of waiting for two consecutive days to buy. In addition, we enter at a worse price when that happens. So, it’s not 100 percent clear which approach should be taken.

If we buy on the first day that $VXST retreats (Table 1), we have to suffer those one-day losses, but if we can get by that, the results for the other holding periods are larger (meaning we bought at a better price on that first day, rather than waiting for the second day as confirmation).

On the other hand, the percentage of winning trades overall is improved by waiting for the second consecutive $VIX close.

In Table 2, the best results are again at 22 days, if you can make it that far. In the post-$VXMT time period (after 11/27/2013), the average trade makes 62.8 $SPX points, or 3.3%.

Time prevented me from running some other statistics and potential variations on this basic theme for this strategy, but that study will be conducted in the near future, and the results will be reported. They would include items such as the following:

Further items to study

First, I would like to summarize the results by the actual trade, regardless of holding period. That should be simple to accomplish. I don’t think it would change the fact that it is more conservative to wait for the second consecutive day, nor would it alter the fact that the 22-day holding period is best – if you can make it that far. But it would give a better overall picture of what the average trade is going to produce.

Second, it might be interesting to see if the term structure has any effect. In other words, if $VXST shoots above the other three indices, and the others are all pointing upwards, is that better or not? My guess is that it would be a better signal, since the term structure is giving a bullish indication for the stock market.

That is what just happened on December 23rd, 2015:

$VXST: 23.05

$VIX: 20.95

$VXV: 21.86

$VXMT: 22.45

So, you can see that $VIX < $VXV < $VXMT – a positive-sloping term structure and one that is bullish for stocks. The next day, $VXST fell back below $VXV and $VXMT, so that would be a buy signal under the system (a la Table 1) on December 16th. The day after that, $VXST remained below all of the others, so that would be a buy signal under the system (a la Table 2) on December 17th.

The next day after that, $SPX was down big on December 18th, but then rallied, so that the Table 2 system was showing a decent profit of 22 $SPX points by December 23rd.

Conversely, if the term structure is sloping downwards when the “alert” goes up (i.e., $VXST > $VIX > $VXV > $VXMT), the market might be in the midst of a bearish free-fall and a buy signal might be more difficult to negotiate.

So that is something we’ll have to test to see if there is a significant difference in results, based on the term structure on the day of the initial trade.

Finally, it might be interesting to see if there is a significant difference in results, depending on where $SPX is on the second consecutive day. That is, if we’re buying at too much of a higher $SPX price than we would have had we just bought on the first day that $VXST crossed back under, should we just skip the trade altogether?

In summary this is an interesting concept that we have quantified to some extent, but we want to do some more work before putting this to use in real trades.

This arcticle was orignally published on 12/28/15 as part of The Option Strategist Newsletter. Receive the articles when they are first published, along with specific trading recommendaitons by subscribing today!

© 2023 The Option Strategist | McMillan Analysis Corporation